While a week does not make a trend and the road to recovery for business and group travel will likely have many ups and downs, the latest weekly performance data from STR shows that demand for hotels is coming back, particularly in the U.S. top 25 markets, where its absence has been very apparent.

The next several weeks will likely cause some anxiousness among hoteliers around those demand segments, but it’s all predictable. Observances of the Jewish holidays Rosh Hashanah and Yom Kippur are expected to have a negative effect on business and group travel, and leisure travel demand will be aided by U.S. school breaks, such as the observance of Columbus/Indigenous Peoples’ Day.

After several consecutive week-over-week declines, typical for this time of year as the travel season transitions from summer to fall, U.S. hotel demand soared back for the week ending Sept. 17. Compared to the previous week, demand was up 13%, while occupancy reached a six-week high of 69.6%.

Weekday occupancy was slightly better at 69.9%, and that metric was even better in the top 25 markets at 75.5%. Weekday top 25 market hotel occupancy has only been higher one other time since March 2020 — in the week of June 18, 2022.

Nominal average daily rate reached a seven-week high of $156, up 5.8% week over week and 18% year over year. Real ADR, adjusted for inflation, was equal to what it was in the same week of 2019. After three weeks below $100, nominal revenue per available room jumped to $108, 19.4% greater than a week ago and 31% higher than in the same week last year. Real RevPAR was just under 2019’s value.

Over the past 22 years, U.S. hotel demand for the first full week after the Labor Day holiday has increased on average by 14.5%.

This year in the week ending Sept. 17, demand was up 13%, on the lower end of the range seen since 2000. The U.S. hotel industry sold 27.2 million room nights, the most ever for a full week after Labor Day. However, due to the calendar shift in the holiday, it was not the highest demand for the 38th week of the year. That record was set in 2019, two weeks after the Labor Day holiday, when the industry sold 8,000 more room nights than this year.

Business and group travel contributed the most to the strong growth in weekday demand.

Weekday demand was the seventh highest since the start of the pandemic. The previous six pandemic-era highs were all achieved during the 2022 summer season when leisure travelers were also filling hotel rooms. Excluding the prime summer travel months of June and July, weekday demand was the highest since the start of the pandemic and the 15th highest of all time going back to 2000.

The U.S. top 25 hotel markets benefited the most from the return of business and group travelers.

Weekday occupancy topped 70% in 18 of the markets with six — Boston, Chicago, Denver, New York, San Francisco and Seattle — surpassing 80%. Seattle and New York led the top 25, both topping 90% occupancy for the week.

Chicago, New York and Seattle hotel markets had their highest weekday demand since the start of the pandemic. Philadelphia also set a pandemic-era record for demand with weekday occupancy at 69%.

Four markets — Houston, Miami, New Orleans and Tampa — were laggards with weekday occupancy in the low-60% range. September is normally the lowest occupancy month for Miami and Tampa, so that is not a surprise, but Houston and New Orleans occupancy tends to go up at this time of year.

Central business district weekday hotel demand and occupancy (79%) was also the highest its been since the start of the pandemic era. Weekday occupancy surpassed 90% in four central business districts — Boston, Chicago, New York Financial District and Seattle. New Orleans had the lowest weekday occupancy of the central business districts at 47%. All other central business districts reported weekday occupancy above 65%, and most were above 70%. Full-week demand and occupancy for the central business districts was 76%, also the highest of the pandemic era.

Weekday group demand was also the highest its been since March 2020, as luxury and upper-upscale hotels sold more than 1.1 million room nights during the week.

Total group demand, all chain scales and classes, accounted for more than a third of the gain in weekday demand and made up 16% of the industry’s total weekday demand.

Weekday occupancy was in the mid-70% range in the predominately business-oriented chain scales — including upper-upscale, upscale and upper-midscale — led by upper-upscale hotels at 79%. Not surprising, upper-upscale hotel demand was the highest its been since the start of the pandemic. More than half of the weekday demand gain by upper-upscale hotels came from increased group demand. Full-week occupancy surpassed 70% in four of the seven chain scales, led by luxury at 73%.

Weekend performance also returned from its post-summer doldrums with occupancy of 77%. Weekend occupancy was slightly higher in the top 25 markets at 78%, with half of the markets reporting occupancy above 80% and all but two above 70%. The highest weekend occupancy among all submarkets was in Gatlinburg and Pigeon Forge in Tennessee, both at 95%.

Weekly real ADR, adjusted for inflation, increased to $135, which was slightly better than in the comparable week of 2019. Weekly top 25 market nominal ADR achieved a pandemic-era high of $189, as did real ADR at $164, reaching its highest level since the first week of December 2019. Weekday nominal ADR in the top 25 markets was even higher at $195 and was the third highest in history. Real weekday ADR topped $169.

With the jump in demand and the continued surge in ADR, nominal RevPAR was above 2019 levels in nearly every market during the week. Half of all markets had weekly Real RevPAR above 2019 including Chicago, Miami, Orlando, San Diego and Phoenix. Among the top 25 markets, Orlando led in comparisons to 2019, with weekday real RevPAR 19% higher.

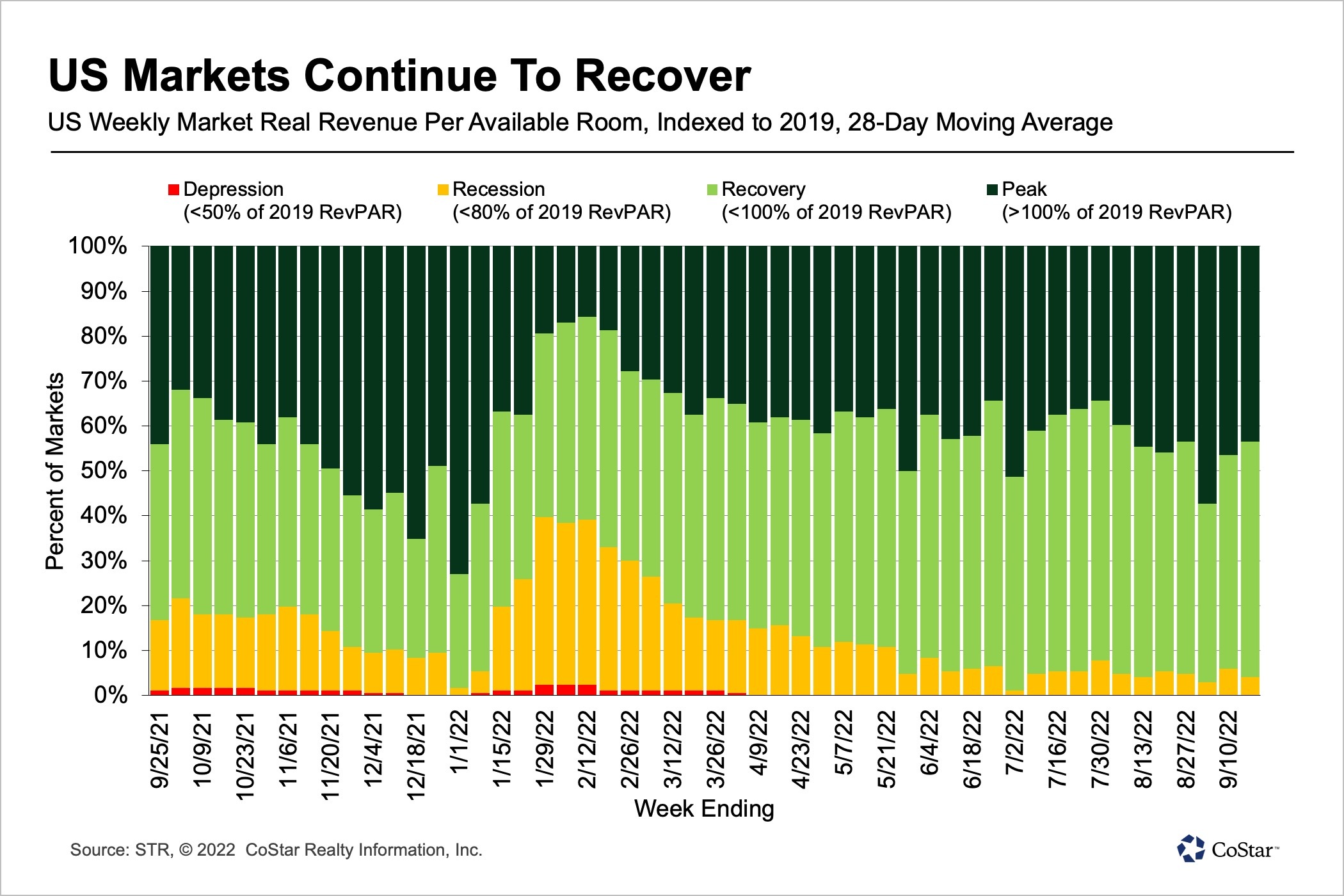

In the 28 days ending Sept. 17, 43% of the 166 STR-defined markets had real RevPAR above 2019. Only two markets, San Jose and San Francisco, were still categorized as being in “recession,” as real RevPAR was less than 80% of what it was in 2019.

Isaac Collazo is VP Analytics at STR.

This article represents an interpretation of data collected by CoStar’s hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.

Return to the Hotel News Now homepage.